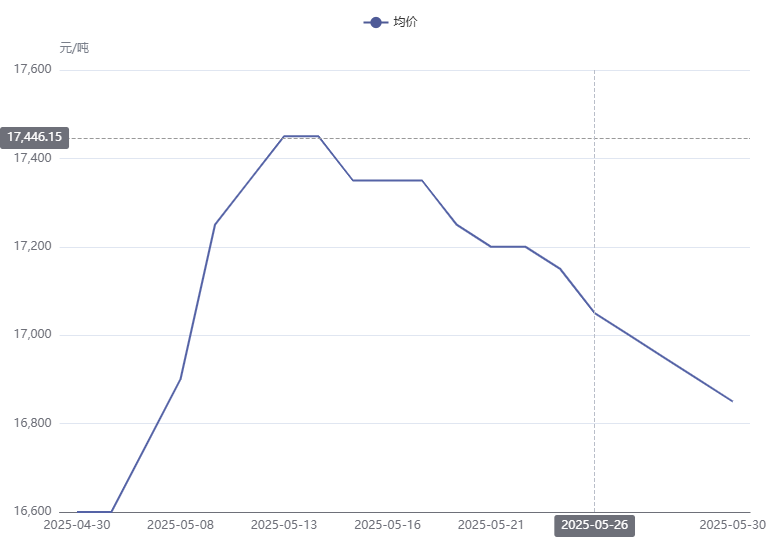

In May, magnesium ingot prices exhibited an inverted V-shaped trend. At the beginning of the month, influenced by market disruptions caused by dolomite production halts, magnesium prices surged abruptly, rising from 16,600 yuan/mt to 17,200 yuan/mt, a two-day leap of 800 yuan/mt, representing a 2.38% increase. By mid-to-late May, as prices continued to climb, purchasers gradually returned to rationality, compounded by small magnesium plants successively offloading goods at lower prices. Consequently, the price center gradually declined. As of the time of writing, the mainstream transaction prices for 99.90% magnesium ingots in major production areas ranged between 16,700-16,800 yuan/mt.

Environmental Protection Checks Team Enters Shaanxi: What Is the Actual Impact on Magnesium Prices?

No sooner had one wave subsided than another arose. As the memory of the dolomite production halt in Wutai, Shanxi, gradually faded among industry participants, the Ministry of Ecology and Environment announced the launch of the third round, fourth batch of central ecological and environmental protection checks in provinces including Shanxi, Inner Mongolia, Shandong, Shaanxi, and Ningxia. These provinces account for 96.3% of total magnesium ingot production, encompassing all major production areas. Will this affect magnesium prices?

According to a representative from a magnesium smelter, due to the environmental protection checks, some smelters have postponed maintenance to July, which may impact newly resumed production in June. However, it has been confirmed that two smelters will resume production in early June, indicating no inevitable correlation between the checks and delayed production resumptions.

May’s Inverted V-Shaped Magnesium Price Trend: What Lies Ahead?

The magnesium ingot market is expected to remain in a tight balance in the short term, with persistently low inventory levels providing underlying support. The room for price pullback is limited. However, as smelters in Xinjiang, Shaanxi, and other provinces gradually resume production, the additional supply may once again increase inventory pressure for smelters. Magnesium ingot prices are projected to fluctuate in June.